Indian Electric Vehicle Market: Growth Outlook, Trends, and Future Opportunities

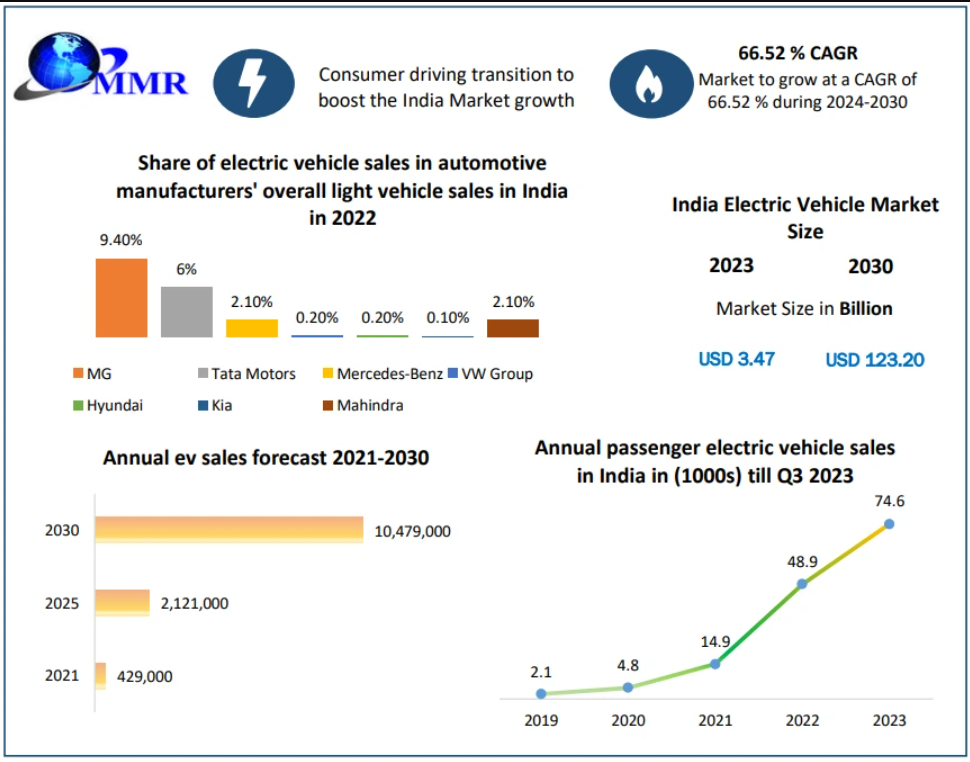

The Indian Electric Vehicle Market was valued at USD 3.47 billion in 2023 and is projected to reach an impressive USD 123.20 billion by 2030, growing at a remarkable CAGR of 66.52% during the forecast period. India is rapidly emerging as a global EV hub, driven by robust policy support, shifting consumer preferences, supply chain localization, and growing environmental awareness.

To know the most attractive segments, click here for a free sample of the report:https://www.maximizemarketresearch.com/request-sample/14886/

Indian Electric Vehicle Market Overview

Electric Vehicles (EVs) operate using electric motors powered by rechargeable batteries or alternative energy sources like fuel cells. They offer zero tailpipe emissions, lower operating costs, and reduced dependence on fossil fuels. The Indian EV landscape comprises:

- Battery Electric Vehicles (BEVs)

- Plug-in Hybrid Electric Vehicles (PHEVs)

- Fuel Cell Electric Vehicles (FCEVs)

The Indian automotive sector—currently the 5th largest globally—is expected to become the 3rd largest by 2030. As India imports nearly 80% of its crude oil, the transition to EVs is crucial for economic and environmental sustainability.

According to the India Energy Storage Alliance (IESA), the Indian EV industry is expected to grow at a 36% CAGR, supported by national policies and a strong governmental push toward net-zero targets by 2070.

NITI Aayog’s EV adoption goals for 2030 include:

- 70% adoption in commercial cars

- 30% in private cars

- 40% in buses

- 80% in two- and three-wheelers

In the past three years, India has registered 0.52 million EVs, indicating strong market momentum.

Regional Landscape

In 2021, the highest EV sales were recorded in:

- Uttar Pradesh – 66,704 units

- Karnataka – 33,302 units

- Tamil Nadu – 30,036 units

UP led the three-wheeler segment, while Karnataka and Maharashtra dominated two-wheeler and four-wheeler sales, respectively.

Market Dynamics

- Consumers Driving India’s EV Transformation

Affordable EV options, particularly below $20,000, have fueled demand. Passenger EV sales doubled in the first nine months of 2023. Key insights:

- 86% of EVs sold cost under $20,000

- India’s EV fleet exceeds 2.3 million, with 90% comprising electric two- and three-wheelers

- Over 50% of three-wheelers registered in 2022 were electric

Urban commuters, ride-hailing services, and delivery fleets are increasingly opting for EVs due to lower running costs.

- Shifting Consumer Preferences

A significant 70% of Indian urban car buyers are considering EVs for their next purchase—higher than the global average. Sustainability plays a key role:

- 75% of Indian consumers are adapting life choices based on sustainability

- Electric two-wheelers rank sustainability among the top three decision factors

- Total cost of ownership (TCO) parity with ICE vehicles is accelerating adoption

- Government Support and Incentives

Key initiatives propelling India’s EV transition include:

- FAME-II Scheme – subsidies for EV purchases & charging infrastructure

- PLI Scheme – Auto & Auto Components – boosts domestic EV and component manufacturing

- PLI Scheme – ACC Battery Storage – supports advanced battery production

- State-level EV policies incentivizing adoption, charging setups, and fleet electrification

Delhi aims to electrify 80% of its public buses by 2025, signaling aggressive regional targets.

- Challenges Restraining Market Growth

Despite promising growth, challenges persist:

- Insufficient charging infrastructure—especially on highways

- High upfront EV cost, affecting price-sensitive buyers

- Battery concerns—longevity, performance, recycling

- Limited domestic supply chain for motors, lithium batteries, and power electronics

- Skilled workforce shortage in EV manufacturing and maintenance

Market Segmentation

By Technology Type

- Battery Electric Vehicles (BEVs) – Dominant segment in 2023

- Growing charging infrastructure

- Strong government incentives

- Improving battery range and reduced costs

- Plug-in Hybrid Electric Vehicles (PHEVs)

- Fuel Cell Electric Vehicles (FCEVs)

By Vehicle Type

- Two-Wheelers – Market Leader (2023)

- Ideal for urban commuting

- Affordable pricing

- Strong presence of Indian startups and brands

- Passenger Cars

- Commercial Vehicles

Market Segment by End User

- Individual Consumers

- Fleet Owners & Operators

- Car Rental Companies

- Others (logistics firms, government fleets, public transport operators)

To know the most attractive segments, click here for a free sample of the report:https://www.maximizemarketresearch.com/request-sample/14886/

Top Indian Electric Vehicle Manufacturers

- Electrotherm (India) Limited

- Hero Electric Vehicles Pvt. Ltd.

- Hyundai Motor India Ltd.

- JBM Group

- Mahindra & Mahindra Limited

- MG Motor India Private Limited

- Okinawa Autotech

- Olectra Greentech Limited

- Omega Seiki Mobility

- Piaggio & C. S.p.A.

- Tata Motors Ltd.

- TVS Motor Company

- VE Commercial Vehicles Limited

These players are expanding portfolios, improving battery technologies, and building strategic charging partnerships.

Noteworthy Industry Developments

| Company | Key Update |

| Kia | Developing small EV SUVs in India for global markets |

| Maruti Suzuki | First India-made EV launching in 2025 |

| Tata Motors | Received USD 678M order for electric buses; planning 10 new EV models |

| Hopcharge | World’s first on-demand doorstep fast-charging service |

| MG Motors | Collaboration with Bharat Petroleum for nationwide charging setup |

| Mahindra & Mahindra | Targeting 16 EV launches by 2027 |

Market Forecast and Opportunities

India’s EV penetration is expected to reach 10–15% by 2030, creating substantial opportunities for:

- Automotive OEMs

- Battery manufacturers

- Charging infrastructure providers

- Fleet operators

- Financial and leasing companies

- Renewable energy integrators

The convergence of affordability, infrastructure expansion, and strong policy support positions India as one of the world’s fastest-growing EV markets.

Conclusion

The Indian Electric Vehicle Market is witnessing a transformational shift. With increasing environmental awareness, attractive pricing, rapid electrification of two- and three-wheelers, and proactive government measures, India is positioned to become a global EV powerhouse by 2030. Addressing infrastructure gaps, battery technology concerns, and supply chain limitations will be crucial to sustaining the market’s extraordinary growth trajectory.